HOW DOES KAISER ULTIMATE HEALTH BUILDER PLAN WORK?

THE 3 PHASES OF KAISER ULTIMATE HEALTH BUILDER PLAN

1st PERIOD: Accumulation Period or The Paying Period (1st to 7th year)

2nd PERIOD: Extended Period or The Growth Period (8th to 20th year)

3rd PERIOD: The Maturity Year/ Long-Term Care Period (21st Year onwards)

1st PERIOD: Accumulation Period or The Paying Period (First 7 Years)

For the first 7 years you will be paying for the plan. During this time, it works like a typical HMO wherein you have an annual benefit usable for hospitalization expenses. These are also a couple of benefits, like:

• Benefit of free Annual Physical Examination after one year of payment.

- Physical Examination, Chest X-Ray, Routine Fecalysis, Routine Urinalysis, Complete Blood Count

- ECG for Members above 35 and Pap Smear for Female Members above 35 years old or as required.

• Benefit of free Dental Check-up and the following;

- Unlimited Dental Check Ups

- Unlimited Simple tooth extraction

- Once A year Free Dental Prophylaxis

- Recementation of jacket, crowns, inlays, on lays and

- Minor adjustment of Dentures

• Term life Insurance (up to age 75) with accidental death and dismemberment riders.

• In-Patient benefits in accredited hospitals except for pre-existing conditions and dreaded diseases, up to plan annual benefit limit.

• Waiver of installment/ Premium due to death/ total and permanent disability.

2nd PERIOD: Extended Period or The Growth Period (next 13 years)

During this phase, you have completed all the payments and all you have to do is wait and let the plan reach its 20th year (maturity) at this point your will have a starting cash value that you can also use for your medical expenses. The money is invested in government and corporate bonds, which are expected to yield 7-10% compound per year.

Comparison to other providers: during this period, the Kaiser plan is still there for your short-term healthcare needs. The money is still growing at this stage and it is at this period when the Kaiser plan starts to step-up and be more competitive with the other healthcare providers.

• Term life Insurance (up to age 75) with accidental death and dismemberment riders.

• Accumulation of unused Health Benefits at 7-10%

• In-Patient and Out-Patient Hospitalization Benefits subject to remaining member accumulated fund.

• Accumulation of unused Health Bonus at 3-13%

3rd Period: The Maturity Year/ Long-Term Care Period (20th Year onwards)

At the plan’s maturity at 20th year, several bonuses will be awarded like the Long-term care benefit and bonus, plus about 85% of the premiums will be returned to you if you didn’t use the plan during the earlier stages, here, the cash value of your investment would also be good as cash- meaning you can use it for anything not just hospitalization and medical expenses.

Comparison to other providers: at this Period, Kaiser stands out because most healthcare providers are already too expensive by the time you reach your 40s or even 60s. On the other hand, your money with Kaiser has already accumulated and depending on the plan you chose, your Total Health Benefits would be upwards of P500,000 all the way to several millions.

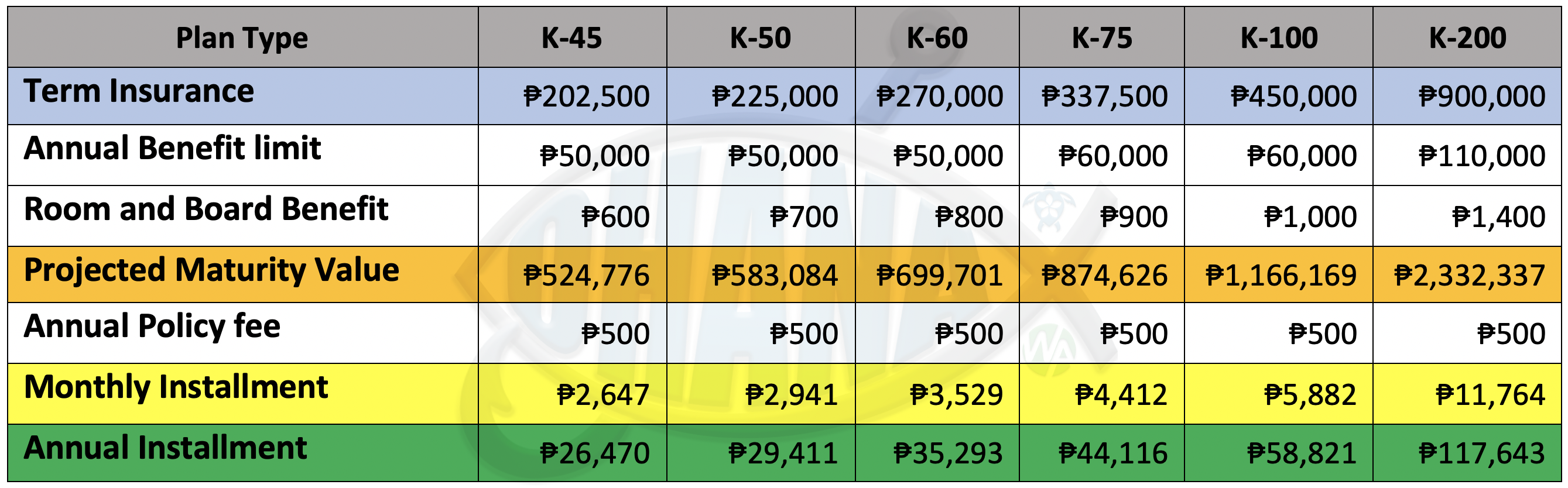

ULTIMATE KAISER HEALTH BUILDER

Pre-Computed Table

Meron kang benefits ng Long term Healthcare na pwede mong magamit khit beyond 100 years old ka na. No traditional HMO will cover you kapag retired ka na, only Kaiser Longterm Healthcare.

Once nag-start ka ng Kaiser, automatic insured ka na ng Term Insurance nito and just in case mawala ang Policy Holder makukuha ng beneficiaries ang Instant Money from the Insurance, Waived na din ang Kaiser Plan, ibig sabihin wala ng iintindihin ang Family. Plus magagamit pa nila yung Health Benefits at makukuha pa nila ang money sa Maturity.

Sa 20th year or sa Maturity makukuha na good as cash ang Investment. Depende sa kukunin na Plan kung magkano ang Maturity nito and option mong kunin ang Fund or Hindi. Kapag ni-retain mo lang ang Funds after the Maturity kumikita pa ito ng average interest rate of 10% per year.

GET YOUR POLICY NOW!

Just click or press on the button link below to get started filling out your Kaiser Online Application Form.

Kaiser International Healthgroup Inc. is registered with Securities and Exchange Commission, Department of Health and Insurance commission

Need our assistance? or do you have any Questions or Clarifications?

Please do not hesitate to contact us anytime if you have any questions or clarifications. If you need any assistance on processing your registration. We are happy to serve you!

ANDREW FABILLAR JR

IMG FINANCIAL COACH

REALYN FABILLAR

IMG FINANCIAL COACH